@narfcake its how poor people stay poor. Buying things on credit- you get far less for your money that way.

Far better to do without and get out of debt and then buy BETTER things for less money. Far better to save up for 18 months (essentially paying yourself a car payment) than it is to buy a car with car payments afterwards. Car payments and other monthly installment plans just keep people poor indefinitely.

@narfcake Reminds me quite a bit of home mortgages. Scary when one realizes how many dollars go into the bank’s coffers (& I got in when interest rates were pretty good! I can’t imagine how awful it must be nowadays!)

… Car payments and other monthly installment plans just keep people poor indefinitely.

@OnionSoup That’s why creditors don’t like folks who know how to do math. But on the other side of the equation, the lack of public transportation in much of the country means that a car is a must – and it needs to be reliable. The sub-$2k option may not be a choice at all, which enters them into the payment loop, which prevents a good chance of saving more money, which locks them in …

@narfcake yeah… Unfortunately for large swaths of the country public transportation isn’t really feasible, but for areas where it is, there really should be a much better effort to create public transportation.

Car payments and other monthly installment plans just keep people poor indefinitely.

Actually it is the buying of items that are out of your price/need range that gets you. A home mortgage on a reasonable house can actually grow wealth.

@chienfou When what you need is priced so that you can’t hope to pay for it up front, the choices get ugly in a hurry. In my entire life, I have had precisely one new car. The rest have been used, often bought cheap because of known issues that I could fix myself. Most people don’t have my options in that area. Without those used vehicles and my skills, I’d have been a pedestrian.

@chienfou@narfcake@OnionSoup

Upkeep, a perpetual subscription fee essentially, is what gets you over time. I owned a house out of state from what I skimmed off my college book costs. Super cheap house and the only direction the land value could go was up.

Turns out, having never set foot on the property to assess and maintain it, I was fined by the city. Given the strong rising value, I figured I could ride it out. Until I couldn’t. While I felt lucky to dump it (and actually did better than break even including all the fees and fines), had I held on for another few years, the price would have spiked. Of course this would have likely meant taking out a loan in the interim, and I wasn’t willing to gamble on how long that would have set me back waiting for the big payday.

The rest have been used, often bought cheap because of known issues that I could fix myself.

@chienfou@werehatrack Zero new cars, and some were purchased without knowing if the issues could be DIY – like my current vehicle which I bought with a “bad” high voltage battery. I knew absolutely nothing about hybrids at the time.

Thankfully, an 8 minute course from the university of YouTube was the solution. Got it started in 25 minutes, much to the surprise of the seller. The OBD scanner still showed a code for a weak battery, though. “Yes, I got it running, but the battery still shows it’s weak. I’m giving you a right of refusal if you don’t want to sell it, but there’s no guarantee how much life it still has either. If you do, it’ll be my problem.”

I’m the second owner, and it’s just shy of 240k miles.

So 9 years after “had to lay 'er down” you’ll still be making payments.

@blaineg A little bit like the associated medical bills, yet somehow so much more painful.

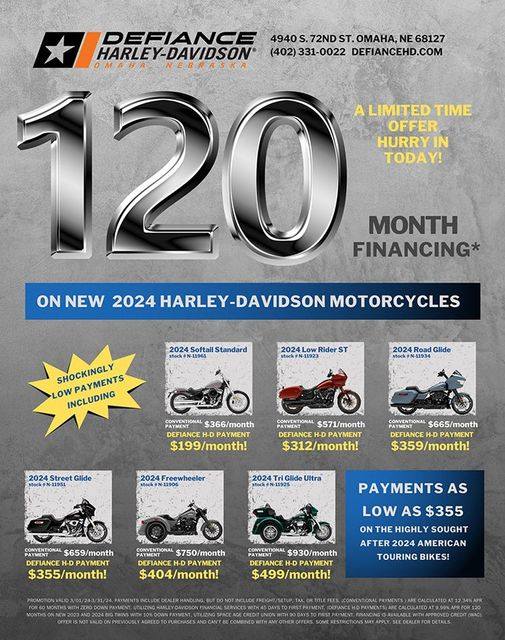

At $199 month, one would be paying nearly $24k for a motorcycle that has a MSRP of $15k.

@narfcake

That’s “interesting”.

@narfcake its how poor people stay poor. Buying things on credit- you get far less for your money that way.

Far better to do without and get out of debt and then buy BETTER things for less money. Far better to save up for 18 months (essentially paying yourself a car payment) than it is to buy a car with car payments afterwards. Car payments and other monthly installment plans just keep people poor indefinitely.

@narfcake Reminds me quite a bit of home mortgages. Scary when one realizes how many dollars go into the bank’s coffers (& I got in when interest rates were pretty good! I can’t imagine how awful it must be nowadays!)

@OnionSoup That’s why creditors don’t like folks who know how to do math. But on the other side of the equation, the lack of public transportation in much of the country means that a car is a must – and it needs to be reliable. The sub-$2k option may not be a choice at all, which enters them into the payment loop, which prevents a good chance of saving more money, which locks them in …

@narfcake yeah… Unfortunately for large swaths of the country public transportation isn’t really feasible, but for areas where it is, there really should be a much better effort to create public transportation.

@narfcake @OnionSoup

Actually it is the buying of items that are out of your price/need range that gets you. A home mortgage on a reasonable house can actually grow wealth.

@chienfou When what you need is priced so that you can’t hope to pay for it up front, the choices get ugly in a hurry. In my entire life, I have had precisely one new car. The rest have been used, often bought cheap because of known issues that I could fix myself. Most people don’t have my options in that area. Without those used vehicles and my skills, I’d have been a pedestrian.

@chienfou @narfcake @OnionSoup

Upkeep, a perpetual subscription fee essentially, is what gets you over time. I owned a house out of state from what I skimmed off my college book costs. Super cheap house and the only direction the land value could go was up.

Turns out, having never set foot on the property to assess and maintain it, I was fined by the city. Given the strong rising value, I figured I could ride it out. Until I couldn’t. While I felt lucky to dump it (and actually did better than break even including all the fees and fines), had I held on for another few years, the price would have spiked. Of course this would have likely meant taking out a loan in the interim, and I wasn’t willing to gamble on how long that would have set me back waiting for the big payday.

@chienfou @werehatrack Zero new cars, and some were purchased without knowing if the issues could be DIY – like my current vehicle which I bought with a “bad” high voltage battery. I knew absolutely nothing about hybrids at the time.

Thankfully, an 8 minute course from the university of YouTube was the solution. Got it started in 25 minutes, much to the surprise of the seller. The OBD scanner still showed a code for a weak battery, though. “Yes, I got it running, but the battery still shows it’s weak. I’m giving you a right of refusal if you don’t want to sell it, but there’s no guarantee how much life it still has either. If you do, it’ll be my problem.”

I’m the second owner, and it’s just shy of 240k miles.